We’ve seen a violent correction in many tech names over the past couple of weeks, and the Nasdaq-100 (QQQ) is now down more than 5% from its highs. However, the size of the correction doesn’t properly highlight the damage underneath the hood of the market. This is evidenced by more than 70% of stocks being below their 50-day moving averages, and nearly 75% of sectors are below their 200-day moving averages. Despite the brief bout of significant selling pressure we’ve seen, there’s still minimal fear out there, with no significant increase in put-buying just yet.

This suggests that the market could certainly head lower before we see a durable bottom. The good news is that the best time to build a shopping list is when the market is in a correction, given that high-quality names can be bought at very reasonable prices. In this update, we’ll look at two names that look set for a strong year ahead and assess their ideal buy-points if this correction continues.

(Source: TC2000.com)

Qualcomm (QCOM) and Paycom Software (PAYC) have little in common, with one company being a human resource and payroll software company, and the former being a Semiconductor name, with the company having its tentacles in several segments, including 5G, Smart Homes, Modem RF Systems, and Processors. Both companies have a history of strong earnings growth and just came off solid quarters, with QCOM growing its quarterly EPS by 76% year-over-year and PAYC reporting 31% quarterly EPS growth. Meanwhile, both names have held up much better than their tech peers, with PAYC and QCOM both above rising 200-day moving averages. Let’s take a closer look at each company below:

Beginning with Qualcomm, the company just had a strong quarter last month, posting a massive top and bottom-line beat, with EPS coming in more than 10% above estimates ($2.55 vs. $2.34). The strong results were helped by 56% growth in handsets, 45% growth in RF front-end, 44% growth in Automotive, and even more impressive 66% growth in IoT. The company noted that the handset growth was driven by strong demand from major original equipment manufacturers, and the company signed a deal with BMW at quarter-end, providing its Snapdragon chip technology to BMW’s automated driving systems.

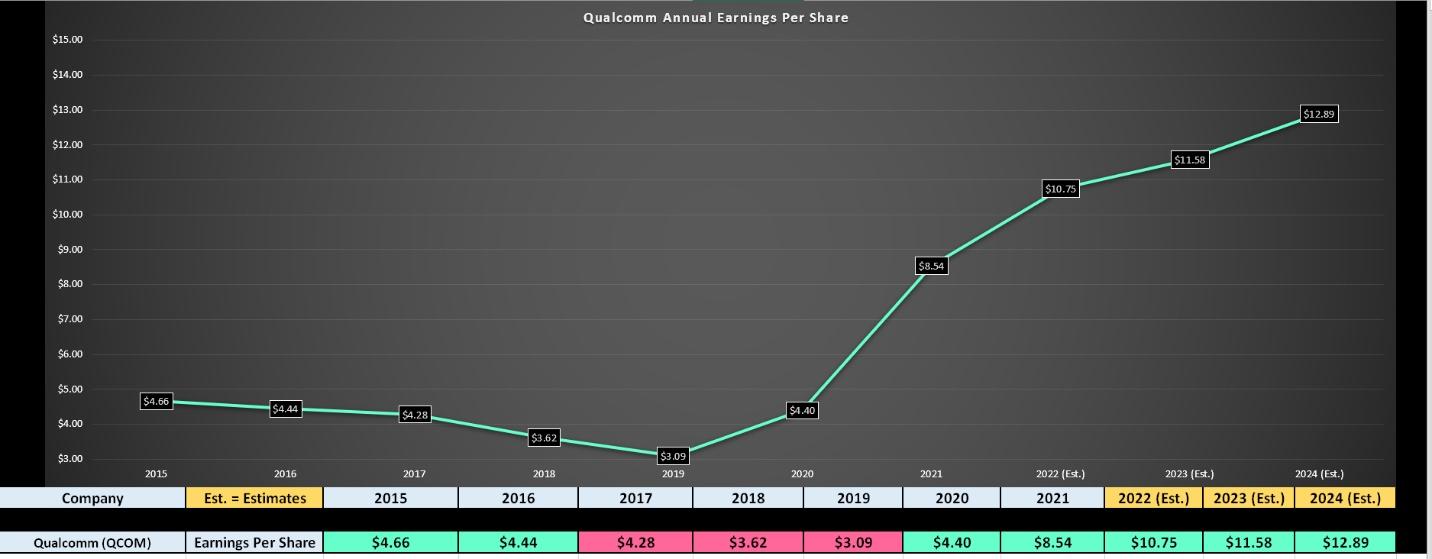

(Source: YCharts.com, Author’s Chart)

While revenue was only up 12% year-over-year, the company saw meaningful margin expansion, boosting annual EPS to $2.55 in fiscal Q4 2021, up from $1.45 in the year-ago period. This translated to 93% growth in annual EPS on a year-over-year basis, and the company is set up for double-digit growth in FY2022 after lapping this massive year. Historically, QCOM has traded at 25x earnings over the past two decades. However, based on FY2023 estimates of $11.58, QCOM is trading at just 15x forward earnings at a share price of $175.00.

This is a very reasonable valuation for a company benefiting from multiple major trends, so it’s not surprising that it appears the stock is being accumulated, given its recent performance and a new all-time high. Even assuming QCOM were to trade at just 22x earnings, below its historical earnings multiple, fair value for the stock would come in above $250.00 per share.

(Source: TC2000.com)

As the chart above shows, QCOM has one of the most attractive looking charts out there currently, with the stock trading above its recent breakout level and above rising monthly moving averages. With the general market currently in a violent correction with a 90% downside volume day on the NYSE last week, I don’t see any reason to chase QCOM here at $175.00. However, if the stock were to pull back below $158.00 and re-test its breakout level, this would present a low-risk buying opportunity. It would also bake in an even further margin of safety. In summary, if this market weakness continues, I would be keeping a close eye on QCOM on a pullback below $158.00.

Moving over to Paycom, the company also had a very strong quarterly recently, with its Q3 revenue up 30% year-over-year, a material acceleration from 12% revenue growth in the year-ago period. The company noted its self-service payroll technology, Beti, is seeing strong demand, with this service allowing employees to do their own payroll. Given the solid Q3 results, Paycom chose to increase its FY2021 guidance to $1.046BB in revenue, which would translate to 24% growth year-over-year.

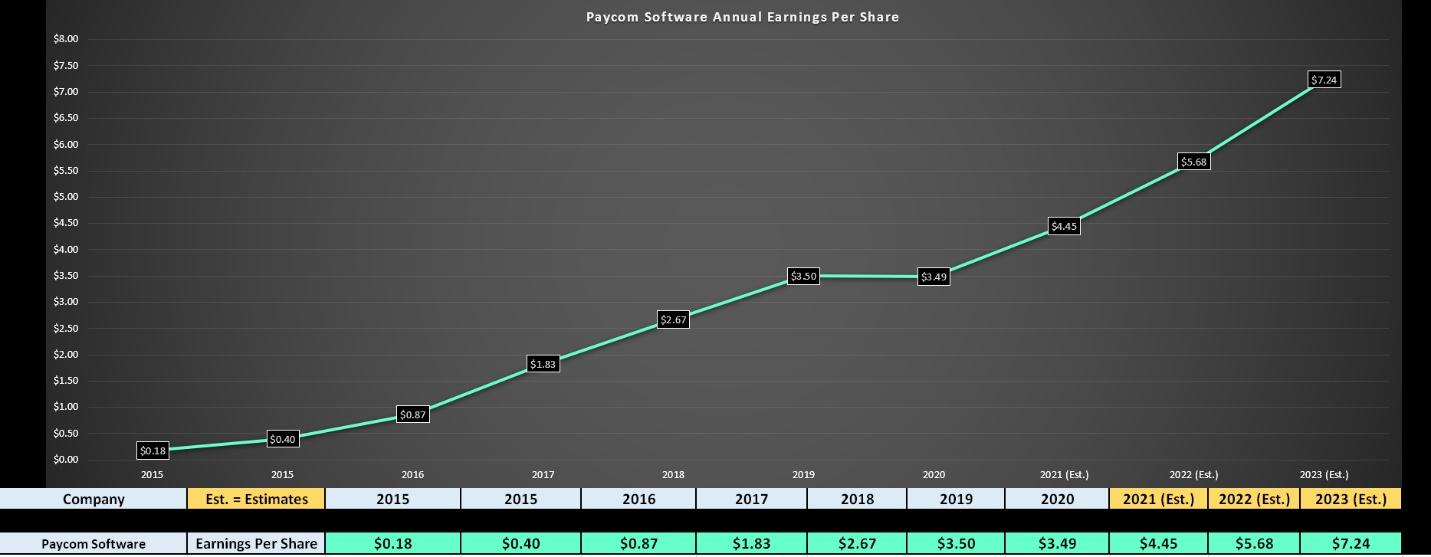

(Source: YCharts.com, Author’s Chart)

Moving over to PAYC’s earnings trend, the company continues to be one of the highest-growth names in the software space, with a compound annual EPS growth rate of ~49% from FY2015 to FY2021 estimates ($4.45 vs. $0.40). However, growth remains robust as we look forward, with PAYC expected to report $5.68 in annual EPS in FY2022 and $7.24 in FY2023. This would translate to 27%, 28%, and 27% growth in annual EPS in FY2021, FY2022, and FY2023, respectively. Given that the company has exceptional margins and more than 97% of its revenue is recurring, it has typically commanded an earnings multiple above 80.

At a current share price of $430.00, PAYC is trading slightly below this level based on FY2023 estimates, with a fair value at an earnings multiple of 75 coming in above $540.00 per share. This points to more than 20% upside from current levels. Generally, I prefer at least a 30% discount to fair value to bake in a meaningful margin of safety, so unlike QCOM, PAYC is not as close to its ideal buy-point. However, if the stock were to dip below $370.00 per share, this would set up an excellent buying opportunity.

(Source: TC2000.com)

If we look at PAYC’s technical chart above, the stock has strong support between $332.00 and $370.00, where buyers stepped in earlier this year, and where the stock’s long-term trend line comes in currently. This corroborates the view that pullbacks towards $370.00 should present low-risk buying opportunities, with a 30% margin of safety relative to PAYC’s fair value of ~$540.00. To summarize, while I don’t see PAYC as a Buy just yet, I would become very interested on a dip below $370.00 per share.

The general market continues to look heavy with multiple distribution days, and breadth continues to deteriorate over the past couple of weeks. If we had a significant amount of fear in the market, this would suggest that we might be near a durable bottom. However, with little fear out there, the odds continue to point to a lower low in the market over the next few weeks. Therefore, I don’t see any reason to rush in and begin buying just yet. Having said that, if QCOM were to dip below $158.00 or PAYC below $370.00 per share, I believe these are two very solid buy-the-dip candidates.

Disclosure: I am short QQQ

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

QCOM shares were trading at $177.50 per share on Thursday afternoon, up $1.87 (+1.06%). Year-to-date, QCOM has gained 18.66%, versus a 23.74% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks to Buy on the Dip appeared first on StockNews.com