In part one of this series, we examined the short-term factors driving the sharpest increase in inflation in three decades, and learned about the reasons that a return to 15% inflation as we saw in the stagflationary 1970s and early 1980s, is highly unlikely.

But while double-digit inflation might be a low probability risk, inflation might end up much higher than we've become accustomed to over the last decade.

Bad News: Higher Inflation Might Be PermanentJust as there are secular trends that are deflationary in nature, there are also those that are inflationary.

Macro 42's Darius Dale, for example, thinks that inflation baseline levels around which future inflation will cycle is now 3%, up from the 1.6% we saw in the 2010s.

Why is that? Several factors.

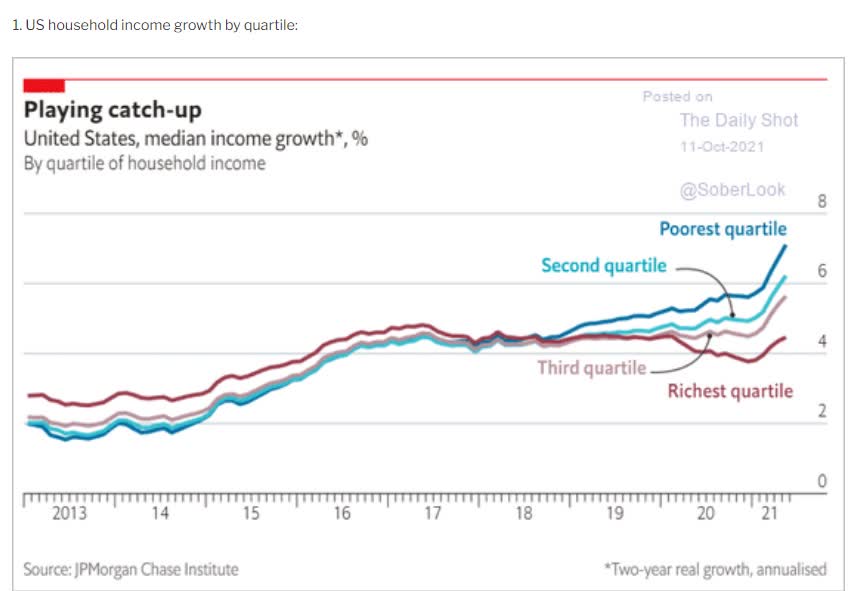

For one thing, the labor shortage created by the "Great Resignation" is likely to persist for several years.

Wages are growing rapidly, 4.2% according to the Atlanta Fed, based on the median 3-month rolling average.

But for the lowest-income Americans its rising as quickly as 7%. And for some industries, like restaurants and hospitality, it's growing at 17%.

Given that the bottom 90% spend 99% of their income that's good news for the economy. But also potentially bad news for rising inflation pressures.

Another secular trend that's likely to push up inflation over time compared to the very low levels of the 2010s is global supply chains.

China joined the World Trade Organization in 2001 and quickly became the factor of the world. Thanks to hundreds of millions of rural Chinese moving to factories in cities, this created a very deflationary rise in global trade.

Post pandemic, companies are diversifying their supply chains away from overreliance on China and some are even returning manufacturing to America.

While that's great from the perspective of more US jobs and less fragile supply chains, it's going to increase production costs for goods.

Several other economists also think that a permanently higher base for inflation is likely.

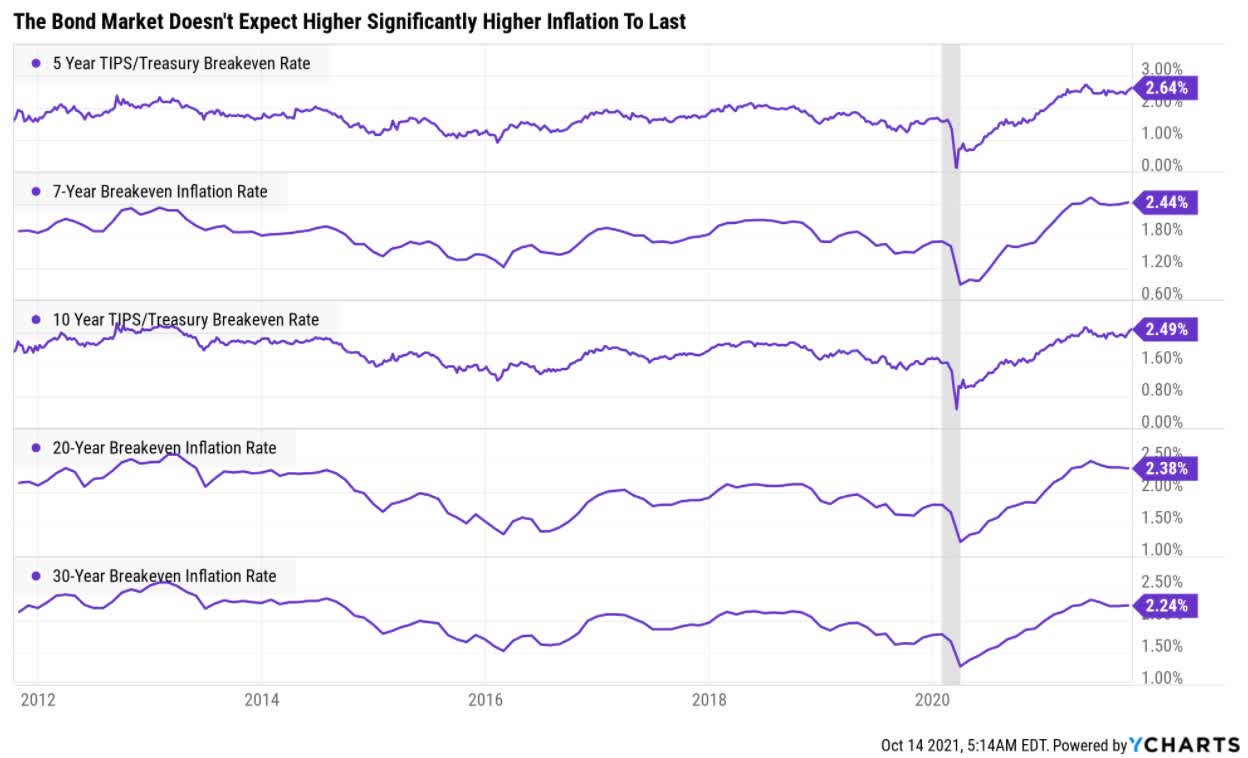

And the bond market agrees.

The bond market thinks long-term inflation will be 2.24% compared to 1.6% in the last decade.

That's not as scary as 3%, but it's very likely to require long-term interest rates to be a lot higher than their current 1.5%.

Good News/Bad News: Higher Inflation Could Result In A Lost Decade For StocksStocks have had a remarkable 10-year run, soaring 340% thanks in part to steadily rising multiples that investors justified with the cry of "there is no alternative" or TINA.

(Source: FactSet Research Terminal)

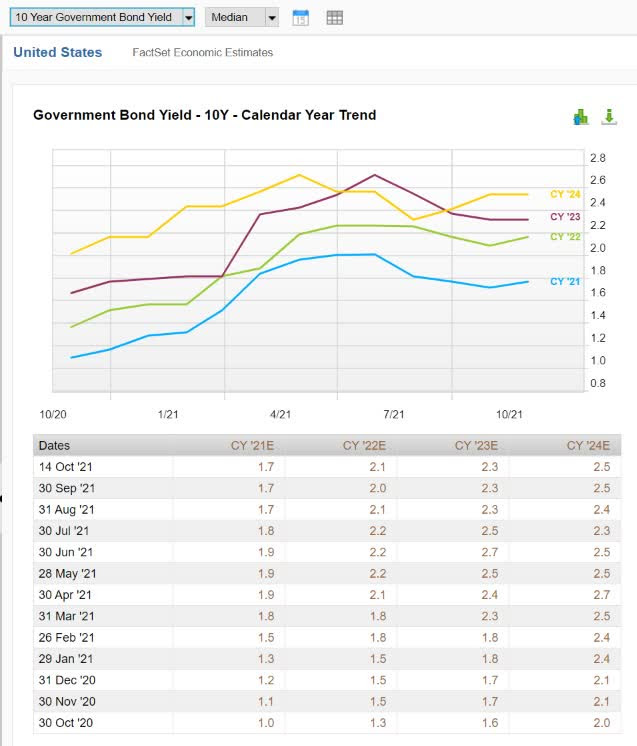

From record lows of 0.5% in August 2020, rates tripled as the economy reopened. And according to the blue-chip economist consensus they are likely to rise another 1% by the end of 2024.

Note that this estimate is up 0.5% over the past year, as inflation has proven to be less transitory than we initially hoped for.

The blue-chip economist consensus range for average 10-year yields for the 2020s is between 2% and 3%. If inflation does in fact, reset higher, to 2.25% to 2.75% or even 3% as some economists expect, then potentially we must prepare for 10-year yields to return to 3% by 2025 or 2026.

Naturally, the popular growth stocks that seemed so "cheap and reasonable" when 10-year yields were 0.5% are likely to suffer significant multiple compression if rates rise by 5X to 6X, or possibly a bit more in the short-term.

Good News: There Are Simple And Effective Waves To Protect Your Portfolio From High Inflation Environments Or Even Profit From ThemI'm not going to sugar coat stagflation, because if we did get roaring inflation rates and soaring interest rates, stocks aren't likely to do well in the short-term.

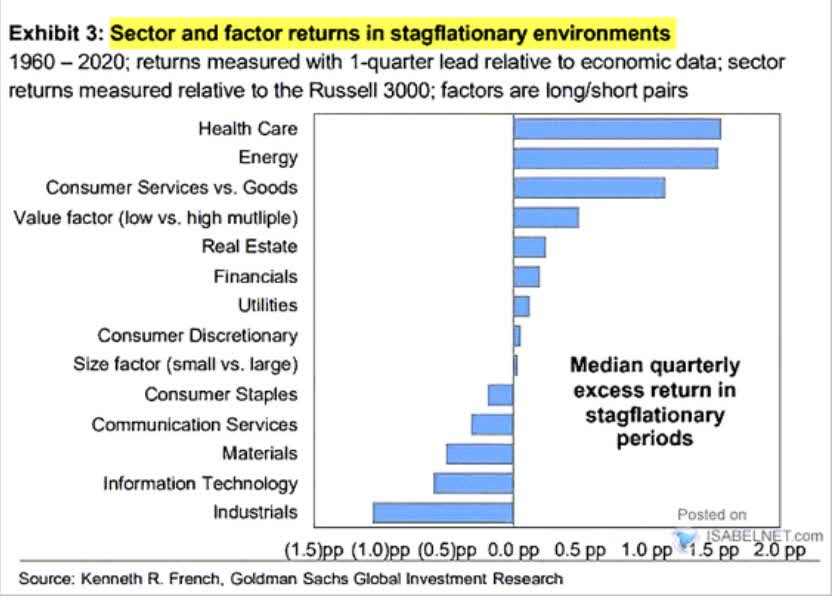

The good news is that certain sectors are more inflation-defensive than others.

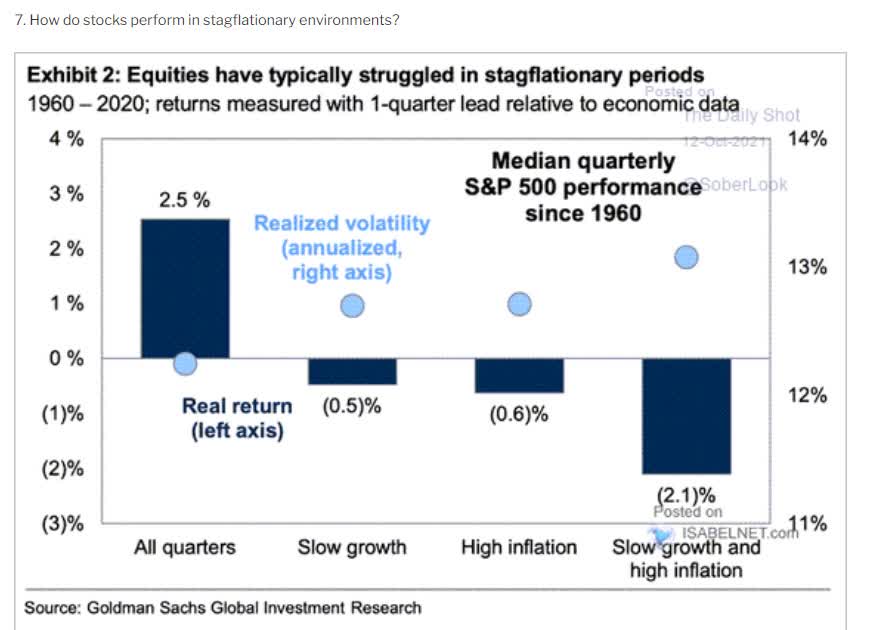

If inflation is running high enough to cause slower or negative economic growth then industrials and materials will be hurt.

Tech, thanks to higher growth and thus higher multiples that are more sensitive to rising rates, also don't tend to do well.

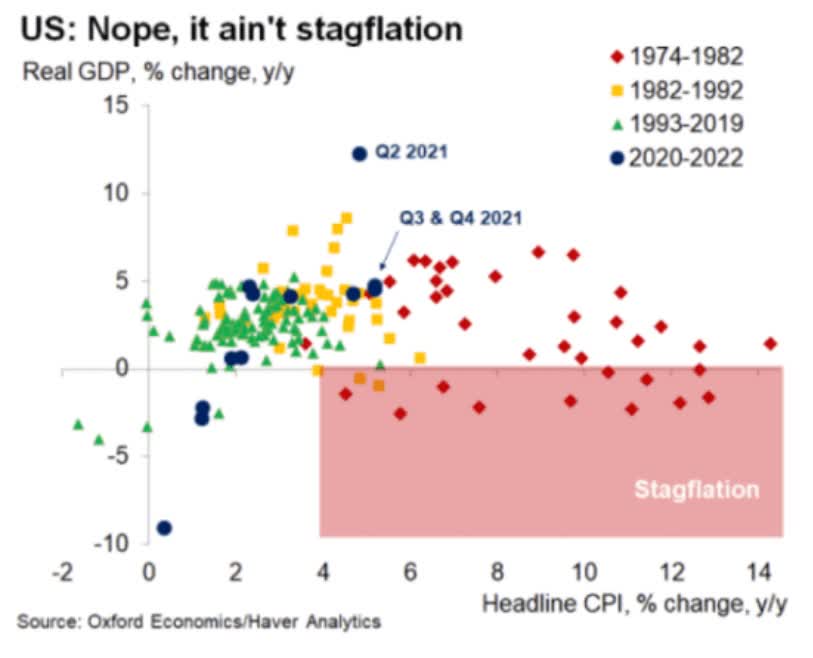

Oxford Economics is rather confident that the strongest growth in 40 years, means we're not seeing stagflation right now, so that should come as a relief to stock investors.

Oxford Economics is rather confident that the strongest growth in 40 years, means we're not seeing stagflation right now, so that should come as a relief to stock investors.

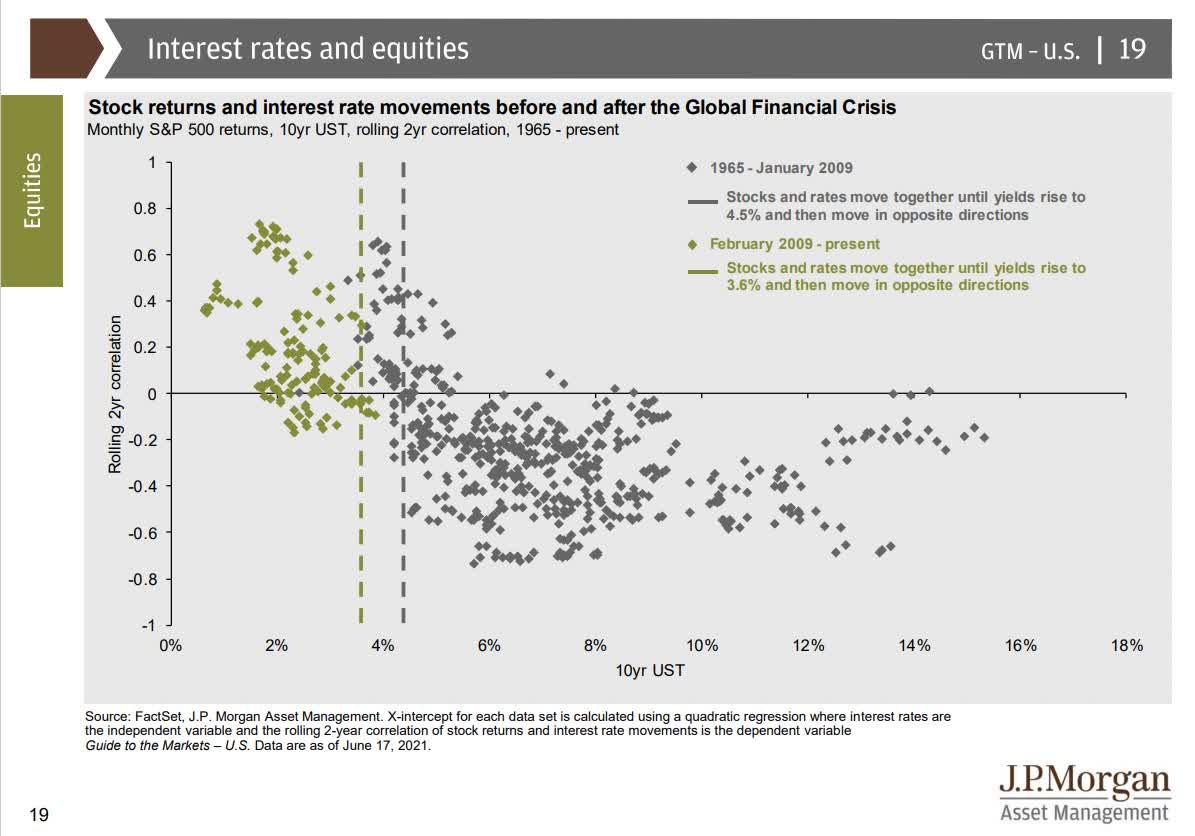

There's also good news that rising interest rates, even in the modern low rate era, don't tend to hurt stocks unless the 10-year yield is above 3.6%.

What if higher debt levels today mean that the tipping point is lower today? It might be. In late 2018 10 year yields hitting 3.25% were one of the catalysts for the December 2018 correction. The one that saw stocks fall 17% in three weeks.

It was also the correction that led to the 31% rally in 2019, the 2nd best year for the market in over three decades.

(Source: JPMorgan Asset Management)

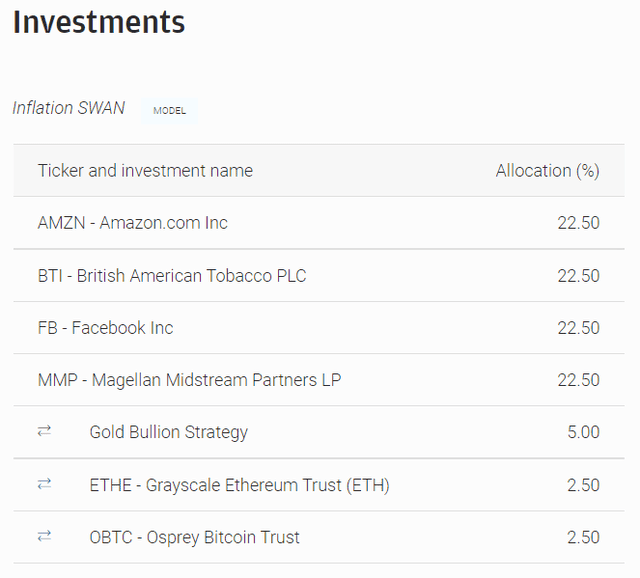

Let's consider a very simple inflation hedged blue-chip portfolio.

It consists of Amazon and Facebook providing hyper-growth at a reasonable price, and British American and Magellan Midstream, the highest safe yield on Wall Street, and relatively inflation defensive as well.

To hedge against inflation, I did a very simple 10% allocation, split 50/50 between gold and the two most popular cryptocurrencies, Bitcoin and Ethereum.

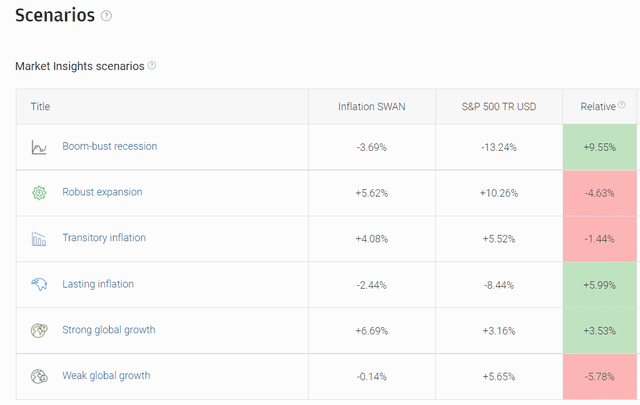

How do the blue-chip economists at JPMorgan expect this balanced approach between value and growth with modest inflation hedging to perform in a higher inflation economy?

(Source: JPMorgan Asset Management)

If we get stagflation, then JPMorgan expects the S&P to fall 13% but our inflation SWAN portfolio (sleep well at night) less than 4%, outperforming by nearly 10%.

If inflation remains 4% for several years, then its expected to outperform by 6%.

If strong global growth occurs as expected, it's expected to outperform the market by 4%.

What if you didn't hedge against inflation at all?

(Source: JPMorgan Asset Management)

The inflation hedges make very little difference because each of these companies was selected for their attractive valuation, and very strong fundamentals and quality. If inflation does hit double-digits then the hedges are likely to perform better, but that's a low probability risk.

In other words, great companies are likely to perform well, even if inflation rises and if the economy falls into a short-term recession.

So what's the bottom line? Inflation is finally here, though we don't really know yet how bad it will get, or for how long.

If you want to hedge your portfolio with alternative assets such as gold or crypto, then go ahead, just remember that such hedging is not likely to make a significant difference if you're focused on the six fundamentals that matter.

Safety, quality, risk-management, yield, growth, and value are the only things that you need to nail down to retire rich and stay rich in retirement.

SPY shares were trading at $451.53 per share on Friday morning, down $2.06 (-0.45%). Year-to-date, SPY has gained 21.95%, versus a % rise in the benchmark S&P 500 index during the same period.

About the Author: Adam Galas

Adam has spent years as a writer for The Motley Fool, Simply Safe Dividends, Seeking Alpha, and Dividend Sensei. His goal is to help people learn how to harness the power of dividend growth investing. Learn more about Adam’s background, along with links to his most recent articles.

The post The Good News and Bad News Investors Need to Know About Inflation: Part 2 appeared first on StockNews.com