It’s been a volatile start to the week for the major market averages, with the S&P-500 (SPY) and Nasdaq-100 Index (QQQ) both sliding more than 3% to start the week on an intra-day basis. While this has left the markets oversold short-term, it has not done much to help valuations for most tech stocks, with the Nasdaq-100 still up more than 120% off the March 2020 lows and some leading tech stocks easily doubling this performance. The good news is that while the market itself remains expensive, as do many QQQ constituents, there are a few names trading at reasonable prices when factoring in their industry-leading growth rates. Two of these names are Paycom Software (PAYC) and Amazon.com (AMZN), with Paycom recently breaking out of a large base and Amazon currently pulling back after a failed breakout earlier this year. While neither is cheap at current levels, they are names worth paying a close eye on if this market correction continues. Let’s take a closer look below:

(Source: TC2000.com)

Paycom Software and Amazon have little in common. One is a large-cap Enterprise-Software company. The other is a mega-cap Internet-Retail company with a cloud-computing platform, Amazon Web Services. However, two traits that each company shares are market leadership with a wide moat, and incredible compound annual earnings per share growth rates. In PAYC’s case, the company has grown earnings at an astounding compound annual rate of ~64% since FY2014. In AMZN’s case, earnings have grown at 101% compound over the past five years (FY2015). While these growth rates can not persist forever, both companies are expecting to double annual EPS again between FY2020 and FY2023, suggesting that their respective growth stories are far from over. This makes them attractive buy-the-dip candidates, especially since they’ve underperformed some of their peers over the past year, so they are nowhere near as extended from a technical basis. Let’s look at Paycom first:

Paycom released its Q2 2021 earnings in August, reporting revenue of $242MM, up 33% year-over-year, representing the strong growth rate in several quarters. This revenue figure included 98% recurring revenue. The robust H1 performance prompted the company to raise its revenue guidance to ~$1.04BB vs. ~$1.02BB previously, and annual EBITDA to $411MM, up from $401MM. Paycom also released Beti, giving its clients increased payroll accuracy while also giving employees full insight into their paycheck, with advanced knowledge of take-home pay. Beti is the industry’s first self-service payroll technology. As of July 6th, Paycom has already sold Beti to more than 1000 new and existing clients, showing strong demand for this new offering.

(Source: YCharts.com, Author’s Chart)

If we look at Paycom’s earnings trend, we can see that annual EPS was down slightly last year ($3.49 vs. $3.50), but this was lapping a 31% increase in the year-ago period. Normally, it would be discouraging to see an earnings trend finally turn negative with a down year after a streak of several increases in a row. However, this is merely an aberration in the long-term trend, as is evidenced by FY2021, FY2022, and FY2023 estimates. As we can see above, FY2021 annual EPS is projected to hit a new high of $4.40, while FY2023 annual EPS is expected to increase to $7.33. This translates to ~110% growth in annual EPS vs. FY2020 levels ($7.33 vs. $3.49), suggesting that Paycom has several strong years ahead of it. So, while PAYC might look expensive at more than 140x FY2020 earnings, it’s much more reasonably valued relative to estimates of $7.33 in FY2023. In fact, ultra high-growth companies like PAYC can easily command earnings multiple of 90 or higher, which would translate to a fair value of $660.00.

(Source: TC2000.com)

Moving to the technical chart, we see that PAYC broke out of a massive 9-month base and was actually up on Monday despite the overall market weakness. While the stock is extended from its 85-week moving average (green line), this moving average is quickly catching up and should be at the $400.00 level by year-end. As is shown above, dips towards this level have provided excellent buying opportunities. So, while I would not be in a rush to chase PAYC near $495.00, the stock would become very interesting if it pulled back inside its base towards the $450.00 level. This is because the stock would be within 10% of its 85-week moving average (strong support) and offer more than 50% upside to its fair value above $600.00, based on an earnings multiple of 90. For this reason, I believe the stock is worth keeping a close eye on if we do see a shake-out between now and year-end below the breakout level.

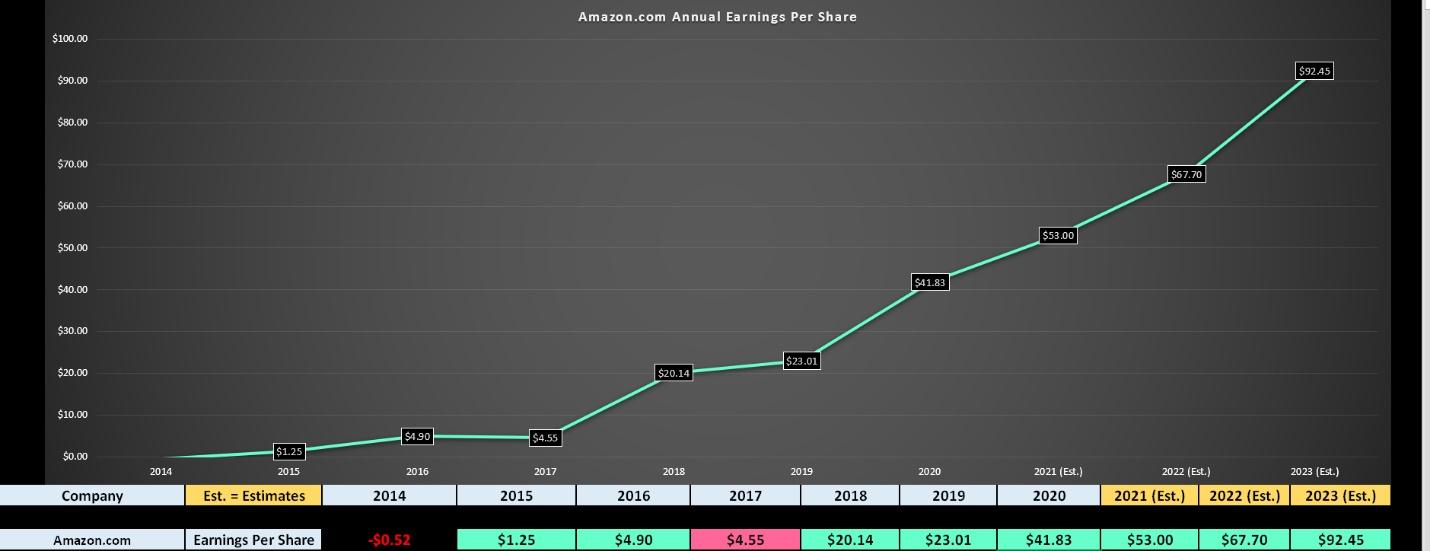

Moving over to AMZN, the company just came off a strong quarter as well, with sales up 27% to $113BB, after lapping 40% growth in the year-ago period. Unfortunately, this wasn’t enough to meet Wall Street’s lofty expectations, with revenue missing by $1.9BB and the company’s Q3 outlook also being a minor disappointment. The good news is that this more than 13% decline in the stock has led to a material improvement in AMZN’s valuation, with the stock now trading at less than 37x FY2023 earnings estimates of $92.45. As we’ve seen in the past, street estimates are generally far too conservative on AMZN, with the company continuously steamrolling competition in new industries and coming out with new innovative ways to steal market share and improve its offerings. If we assume a more likely annual EPS figure of ~$100.00 in FY2023, AMZN is trading at less than 34x forward earnings, a dirt-cheap valuation for a tech juggernaut.

(Source: YCharts.com, Author’s Chart)

While there’s no reason to assign a triple-digit earnings multiple for AMZN as it has typically commanded in its highest-growth years (average of 127), an earnings multiple of 50 is more than reasonable for this high-growth name. Under this assumption, AMZN’s fair value based on FY2023 earnings estimates of $92.45 comes in at $4,622, translating to nearly 40% upside from current levels. As noted above, this assumes only a meet on annual EPS and not a beat. Under the more bullish scenario, with FY2023 annual EPS of $100.00, or a less than 10% beat, AMZN’s fair value jumps to $5,000 per share. This points to significant upside for the stock and suggests that further weakness should present a buying opportunity.

(Source: TC2000.com)

If we look at a technical chart of AMZN above, we can see that the stock looks to be in the middle stages of its new multi-year trend, with the most recent multi-year base preceding a more than 3-year rally in the stock. With the most recent breakout occurring in Q2 2020, AMZN could have another 18 months of upside ahead of it, and pullbacks within this multi-year trend should provide excellent buying opportunities. Looking at clues from the prior multi-year bull market that followed a multi-year base breakout, AMZN rode its 16-period monthly moving average within this 3-year bull market, with any pullback below this moving average presenting a buying opportunity. Currently, AMZN is sitting just 10% above this moving average, suggesting that any pullbacks below $3,000 would present excellent buying opportunities. Obviously, there’s no guarantee that the stock pulls back this sharply, but this would be a low-risk entry point and an area where I would consider adding to my position.

With the general markets only just beginning a short-term correction and complacency still at elevated levels, I don’t see any reason to rush into stocks and hit the asks. Instead, I believe patience is the best move and that investors should look at building shopping lists to prepare for a potential test of the 200-day moving average on the S&P-500. If this were to occur before year-end, this would setup up excellent buying opportunities on AMZN below $3,000, and PAYC below $450.00. In summary, I see AMZN and PAYC as names to keep a close eye on, and I may look to add exposure to both names if this correction in the general market continues, and these stocks test their low-risk buy points.

Disclosure: I am long AMZN

Disclaimer: Taylor Dart is not a Registered Investment Advisor or Financial Planner. This writing is for informational purposes only. It does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Taylor Dart expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

AMZN shares were unchanged in after-hours trading Tuesday. Year-to-date, AMZN has gained 2.66%, versus a 16.74% rise in the benchmark S&P 500 index during the same period.

About the Author: Taylor Dart

Taylor has over a decade of investing experience, with a special focus on the precious metals sector. In addition to working with ETFDailyNews, he is a prominent writer on Seeking Alpha. Learn more about Taylor’s background, along with links to his most recent articles.

The post 2 Tech Stocks to Buy on Dips Before Q4 appeared first on StockNews.com