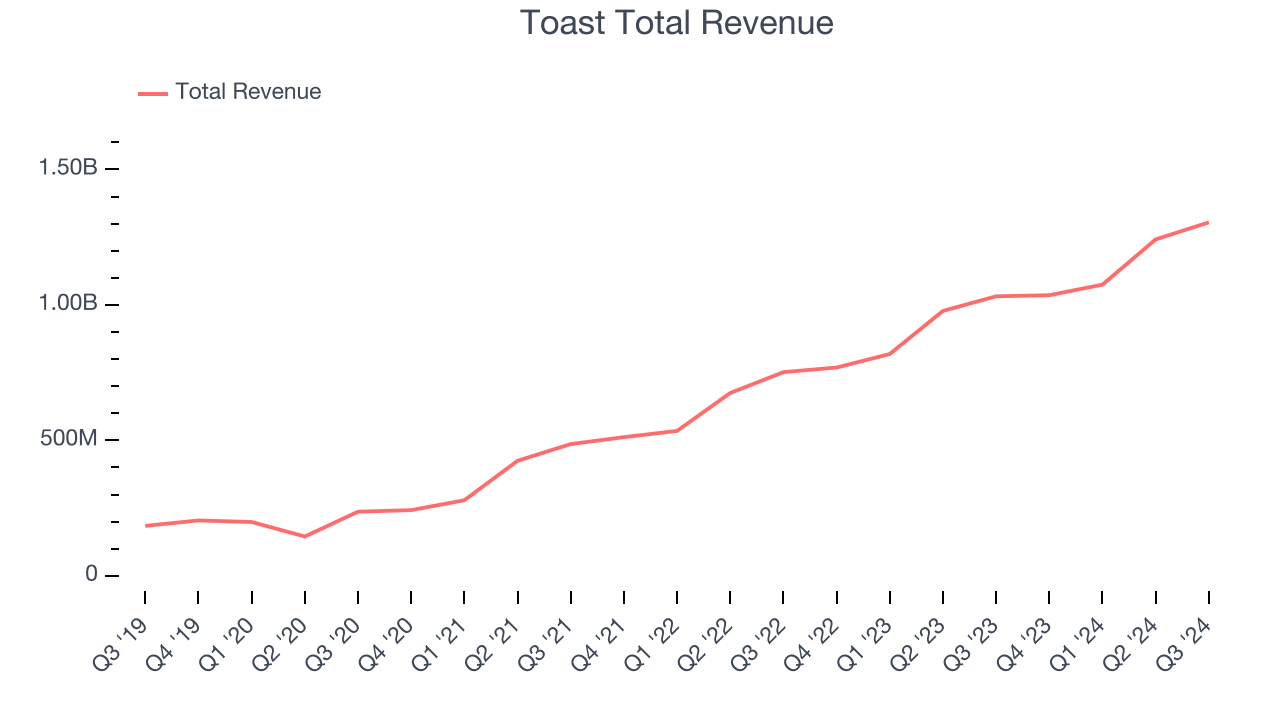

Restaurant software platform Toast (NYSE:TOST) met Wall Street’s revenue expectations in Q3 CY2024, with sales up 26.5% year on year to $1.31 billion. Its GAAP profit of $0.07 per share was 392% above analysts’ consensus estimates.

Is now the time to buy Toast? Find out by accessing our full research report, it’s free.

Toast (TOST) Q3 CY2024 Highlights:

- Revenue: $1.31 billion vs analyst estimates of $1.29 billion (in line)

- EPS: $0.07 vs analyst estimates of $0.01 ($0.06 beat)

- EBITDA: $113 million vs analyst estimates of $78.53 million (43.9% beat)

- EBITDA guidance for the full year is $357 million at the midpoint, above analyst estimates of $305.2 million

- Gross Margin (GAAP): 24.7%, up from 22% in the same quarter last year

- Operating Margin: 2.6%, up from -5.7% in the same quarter last year

- EBITDA Margin: 8.7%, up from 3.4% in the same quarter last year

- Free Cash Flow Margin: 7.4%, down from 8.7% in the previous quarter

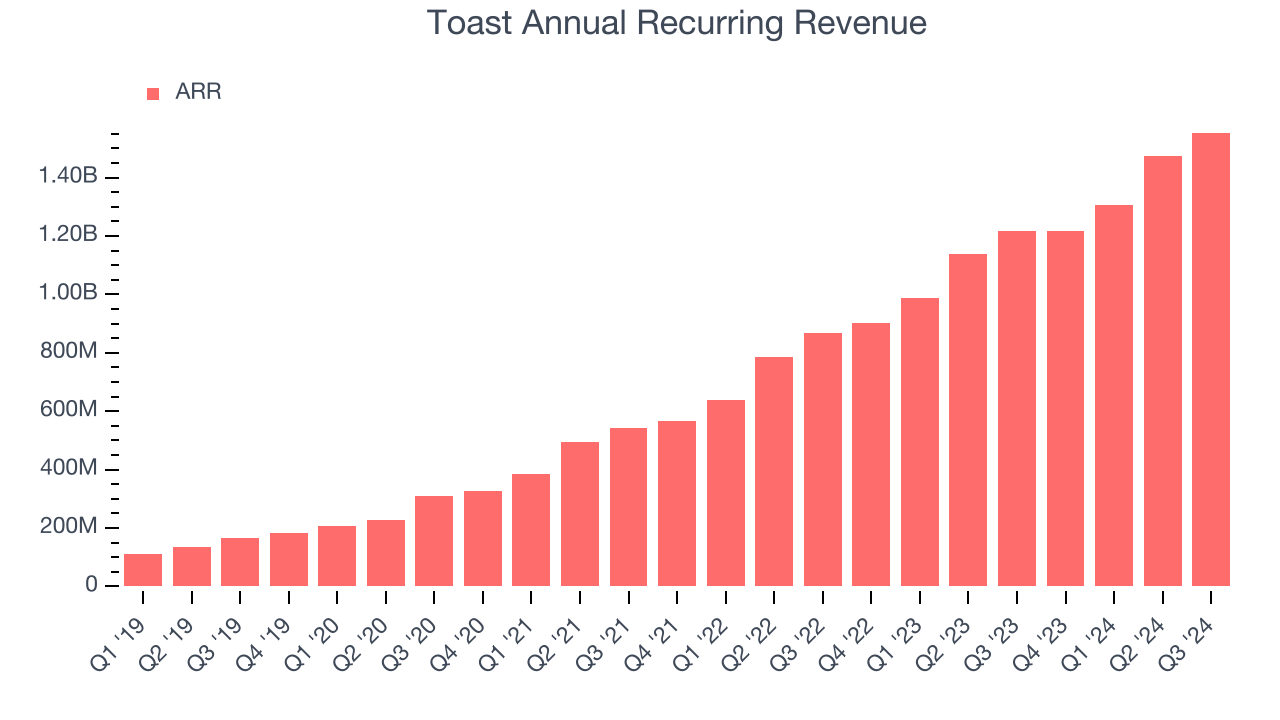

- Annual Recurring Revenue: $1.55 billion at quarter end, up 27.6% year on year

- Market Capitalization: $18.06 billion

“Toast delivered a strong third quarter, adding approximately 7,000 net new locations, growing our recurring gross profit streams1 35%, and achieving Adjusted EBITDA of $113 million. We are well positioned to finish out the year strong and carry this momentum into 2025. Our differentiated vertical software platform is at the foundation of that success, and we continue to innovate to deliver more value to our customers: this fall we launched new products like Branded Mobile App and SMS Marketing alongside over a dozen feature updates,” said Toast CEO and Co-Founder Aman Narang.

Company Overview

Founded by three MIT engineers at a local Cambridge bar, Toast (NYSE:TOST) provides integrated point-of-sale (POS) hardware, software, and payments solutions for restaurants.

Hospitality & Restaurant Software

Enterprise resource planning (ERP) and customer relationship management (CRM) are two of the largest software categories dominated by the likes of Microsoft, Oracle, and Salesforce.com. Today, the secular trend of mass customization is driving vertical software that customizes ERP and CRM functions for specific industry requirements. Restaurants are a prime example where a set of customized software providers have sprung up in recent years to create unique operating systems that blend tax and accounting software, order management and delivery, along with supply chain management. Hotels and other hospitality providers are another example.

Sales Growth

A company’s long-term performance is an indicator of its overall business quality. While any business can experience short-term success, top-performing ones enjoy sustained growth for multiple years. Over the last three years, Toast grew its sales at an incredible 48.1% compounded annual growth rate. This is encouraging because it shows Toast’s offerings resonate with customers, a helpful starting point.

This quarter, Toast’s year-on-year revenue growth of 26.5% was excellent, and its $1.31 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 23% over the next 12 months, a deceleration versus the last three years. Still, this projection is noteworthy and shows the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Annual Recurring Revenue

Investors interested in Toast should track its annual recurring revenue (ARR) in addition to reported revenue. While reported revenue for a SaaS company can include low-margin items like implementation fees, ARR is a sum of the next 12 months of contracted revenue purely from software subscriptions, or the high-margin, predictable revenue streams that make SaaS businesses so valuable.

Over the last year, Toast’s ARR growth has been fantastic, averaging 31% year-on-year increases and punching in at $1.55 billion in the latest quarter. This performance was in line with its revenue growth and shows that customers are willing to take multi-year bets on the company’s technology. Its growth also makes Toast a more predictable business, a tailwind for its valuation as investors typically prefer businesses with recurring revenue.

Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

It’s relatively expensive for Toast to acquire new customers as its CAC payback period checked in at 101.6 months this quarter. The company’s performance indicates that it operates in a competitive market and must continue investing to maintain its growth trajectory.

Key Takeaways from Toast’s Q3 Results

We were impressed by Toast’s optimistic EBITDA forecast for next quarter, which blew past analysts’ expectations. We were also glad its gross margin improved. On the other hand, its ARR (annual recurring revenue) missed analysts’ expectations. Zooming out, we think this was a solid quarter. The stock traded up 20.7% to $39.42 immediately after reporting.

Sure, Toast had a solid quarter, but if we look at the bigger picture, is this stock a buy? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.