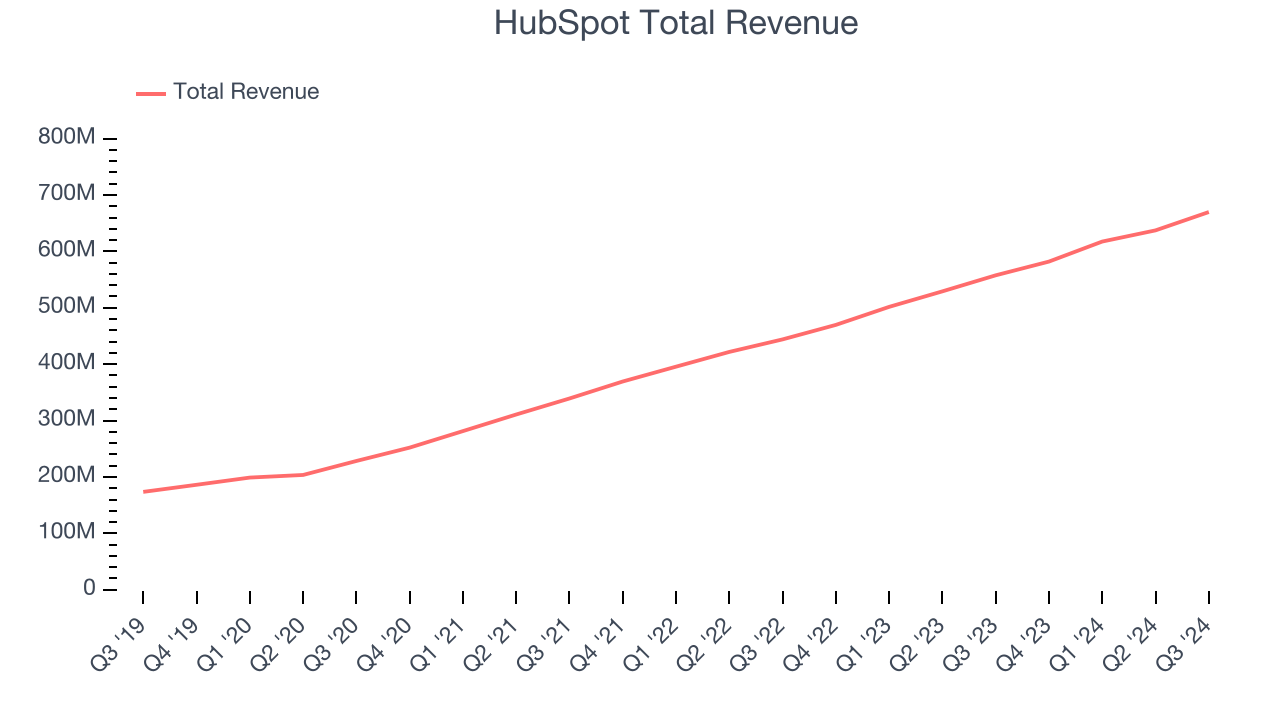

Sales and marketing software maker HubSpot (NYSE:HUBS) announced better-than-expected revenue in Q3 CY2024, with sales up 20.1% year on year to $669.7 million. The company expects next quarter’s revenue to be around $673 million, close to analysts’ estimates. Its non-GAAP profit of $2.18 per share was also 14.2% above analysts’ consensus estimates.

Is now the time to buy HubSpot? Find out by accessing our full research report, it’s free.

HubSpot (HUBS) Q3 CY2024 Highlights:

- Revenue: $669.7 million vs analyst estimates of $647.3 million (3.5% beat)

- Adjusted EPS: $2.18 vs analyst estimates of $1.91 (14.2% beat)

- Revenue Guidance for Q4 CY2024 is $673 million at the midpoint, roughly in line with what analysts were expecting

- Management raised its full-year Adjusted EPS guidance to $7.99 at the midpoint, a 4.2% increase

- Gross Margin (GAAP): 85.2%, in line with the same quarter last year

- Operating Margin: -1.4%, up from -3.3% in the same quarter last year

- Free Cash Flow Margin: 18.6%, up from 13.8% in the previous quarter

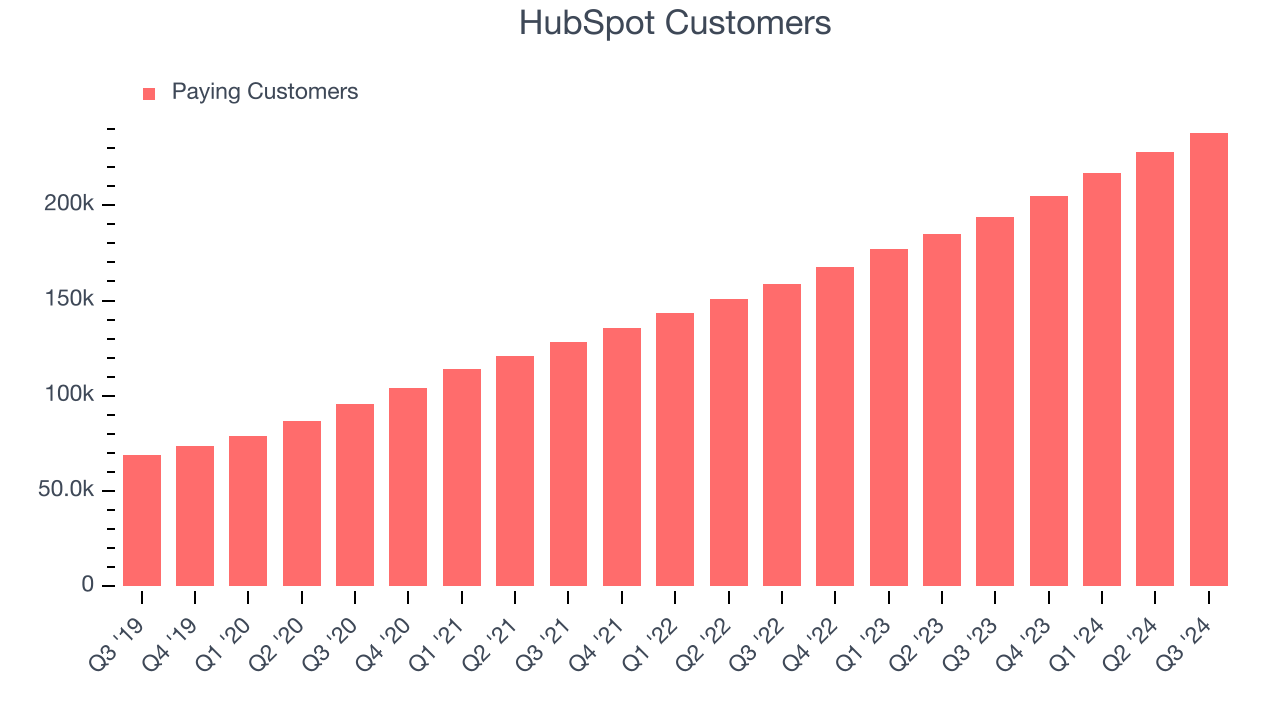

- Customers: 238,128, up from 228,054 in the previous quarter

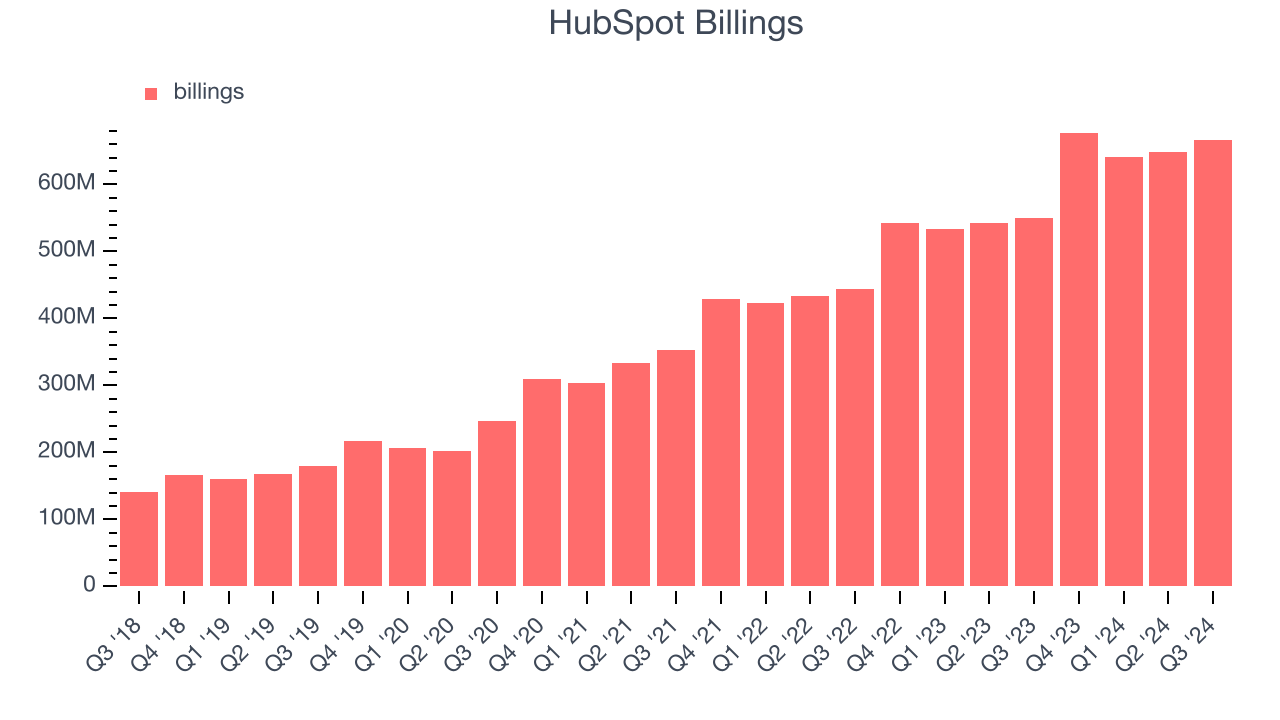

- Billings: $666.5 million at quarter end, up 21.3% year on year

- Market Capitalization: $29.69 billion

Company Overview

Started in 2006 by two MIT grad students, HubSpot (NYSE:HUBS) is a software-as-a-service platform that helps small and medium-sized businesses market themselves, sell, and get found on the internet.

Sales Software

Companies need to be able to interact with and sell to their customers as efficiently as possible. This reality coupled with the ongoing migration of enterprises to the cloud drives demand for cloud-based customer relationship management (CRM) software that integrates data analytics with sales and marketing functions.

Sales Growth

Examining a company’s long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, HubSpot’s sales grew at an impressive 28.4% compounded annual growth rate over the last three years. This is encouraging because it shows HubSpot’s offerings resonate with customers, a helpful starting point.

This quarter, HubSpot reported robust year-on-year revenue growth of 20.1%, and its $669.7 million of revenue topped Wall Street estimates by 3.5%. Management is currently guiding for a 15.7% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 14.5% over the next 12 months, a deceleration versus the last three years. Still, this projection is admirable and illustrates the market is baking in success for its products and services.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Billings

In addition to revenue, billings is a non-GAAP metric that sheds additional light on HubSpot’s business quality. Billings is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Over the last year, HubSpot’s billings growth has been impressive, averaging 21.5% year-on-year increases and punching in at $666.5 million in the latest quarter. This performance was in line with its revenue growth, indicating robust customer demand and a strong sales pipeline. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

Customer Growth

HubSpot reported 238,128 customers at the end of the quarter, an increase of 10,074 from the previous quarter. That’s a little slower customer growth than last quarter but in line with what we’ve observed in past quarters, suggesting that the company still has decent sales momentum.

Key Takeaways from HubSpot’s Q3 Results

We were impressed by HubSpot’s optimistic full-year EPS forecast, which blew past analysts’ expectations. We were also excited its billings outperformed Wall Street’s estimates. On the other hand, its customer growth was a little slower. Overall, we think this was still a very solid quarter with some key areas of upside. The stock traded up 8.7% to $650 immediately following the results.

HubSpot may have had a good quarter, but does that mean you should invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.