Industrial technology company Fortive (NYSE:FTV) fell short of the market’s revenue expectations in Q3 CY2024 as sales rose 2.7% year on year to $1.53 billion. The company expects next quarter’s revenue to be around $1.64 billion, slightly below analysts’ estimates. Its non-GAAP profit of $0.97 per share was 4.2% above analysts’ consensus estimates.

Is now the time to buy Fortive? Find out by accessing our full research report, it’s free.

Fortive (FTV) Q3 CY2024 Highlights:

- Revenue: $1.53 billion vs analyst estimates of $1.55 billion (1.2% miss)

- Adjusted EPS: $0.97 vs analyst estimates of $0.93 (4.2% beat)

- Revenue Guidance for Q4 CY2024 is $1.64 billion at the midpoint, below analyst estimates of $1.65 billion

- Management slightly raised its full-year Adjusted EPS guidance to $3.86 at the midpoint

- Gross Margin (GAAP): 60%, in line with the same quarter last year

- Operating Margin: 19.3%, in line with the same quarter last year

- Free Cash Flow Margin: 28.1%, up from 25.7% in the same quarter last year

- Market Capitalization: $26.14 billion

James A. Lico, President and Chief Executive Officer, stated, “Fortive generated strong operating performance in the third quarter, with better than expected earnings and free cash flow. Our portfolio of high-quality businesses is delivering consistent and more profitable growth, evidenced by robust recurring revenue growth in Intelligent Operating Solutions and Advanced Healthcare Solutions. We are also pleased with the positive momentum in orders growth across all our segments, including double-digit orders growth in Precision Technologies in the third quarter.”

Company Overview

Taking its name from the Latin root of "strong", Fortive (NYSE:FTV) manufactures products and develops industrial software for numerous industries.

Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

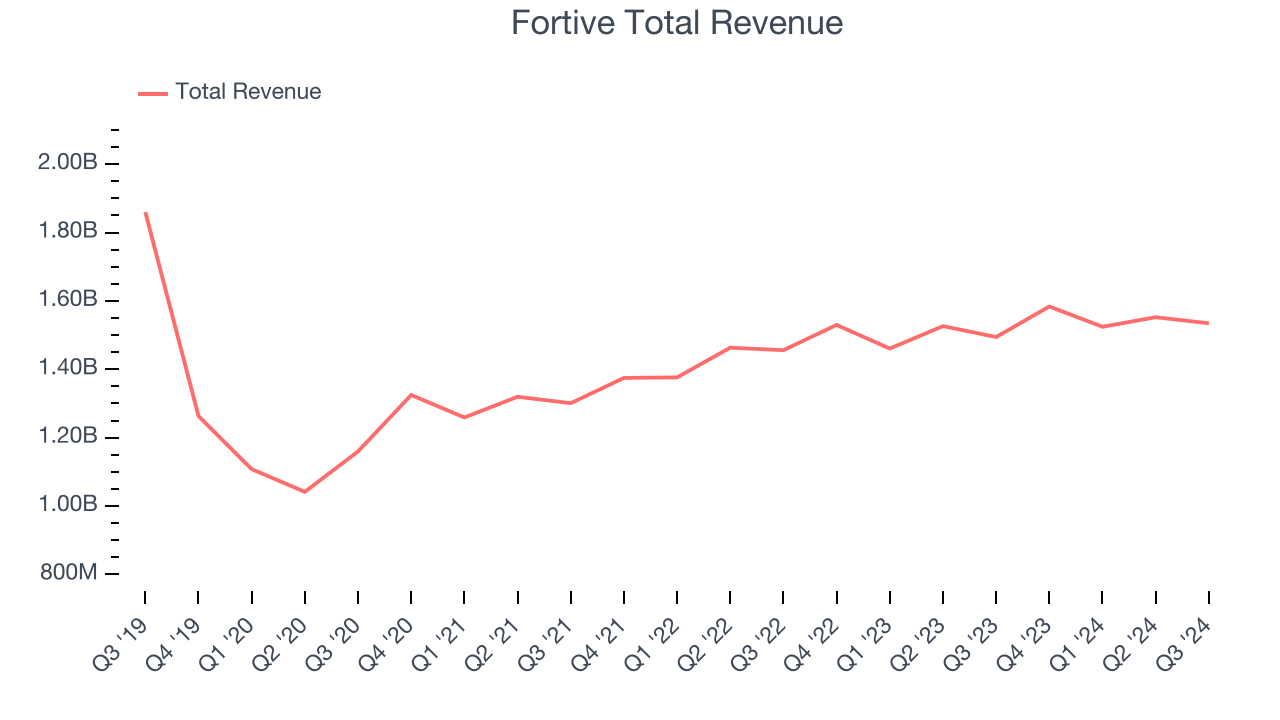

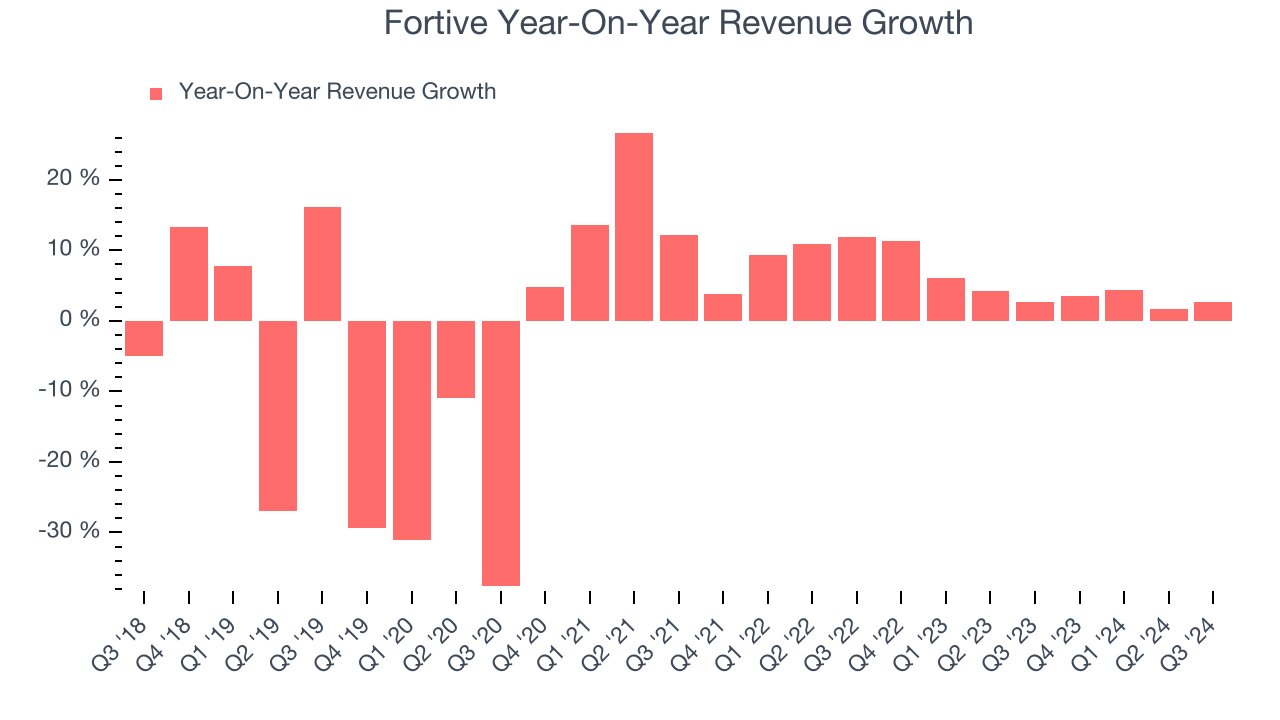

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Fortive’s demand was weak over the last five years as its sales were flat, a poor baseline for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Fortive’s annualized revenue growth of 4.5% over the last two years is above its five-year trend, but we were still disappointed by the results.

This quarter, Fortive’s revenue grew 2.7% year on year to $1.53 billion, falling short of Wall Street’s estimates. Management is currently guiding for a 3.6% year-on-year increase next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 5.3% over the next 12 months, similar to its two-year rate. This projection is underwhelming and shows the market believes its newer products and services will not accelerate its top-line performance yet.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

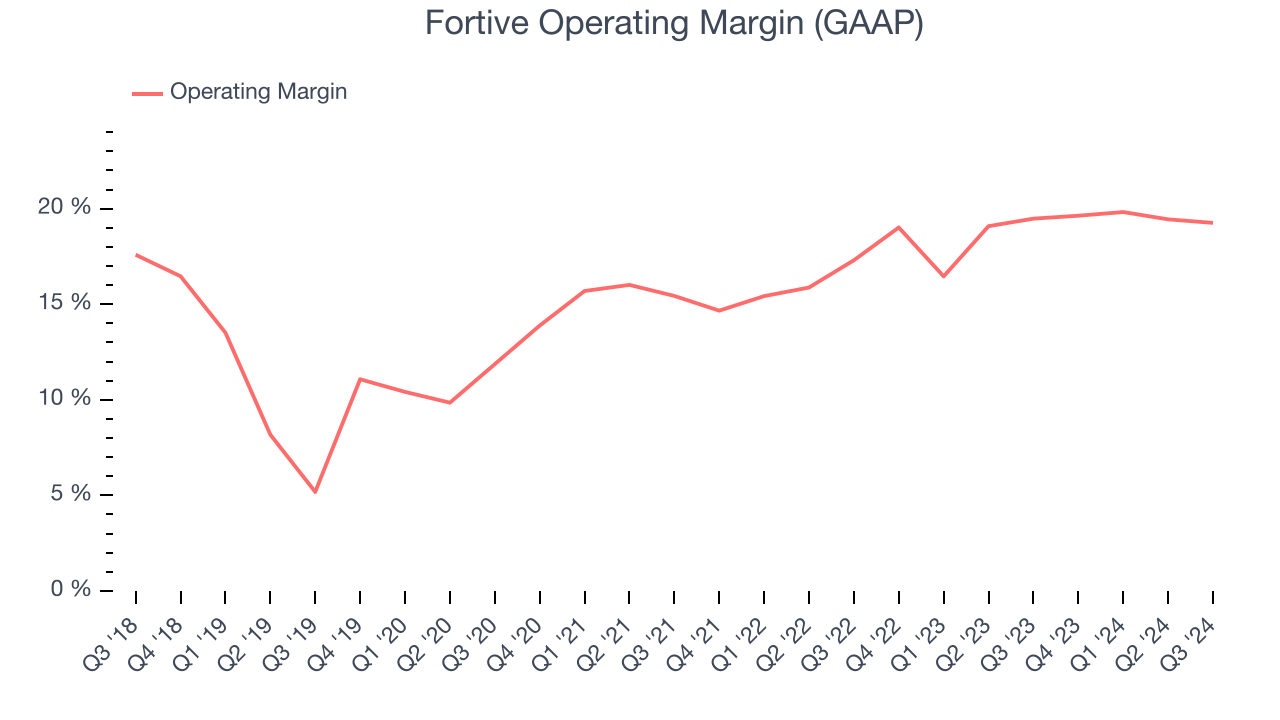

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Fortive has been a well-oiled machine over the last five years. It demonstrated elite profitability for an industrials business, boasting an average operating margin of 16.3%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Fortive’s annual operating margin rose by 8.7 percentage points over the last five years, showing its efficiency has meaningfully improved.

This quarter, Fortive generated an operating profit margin of 19.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

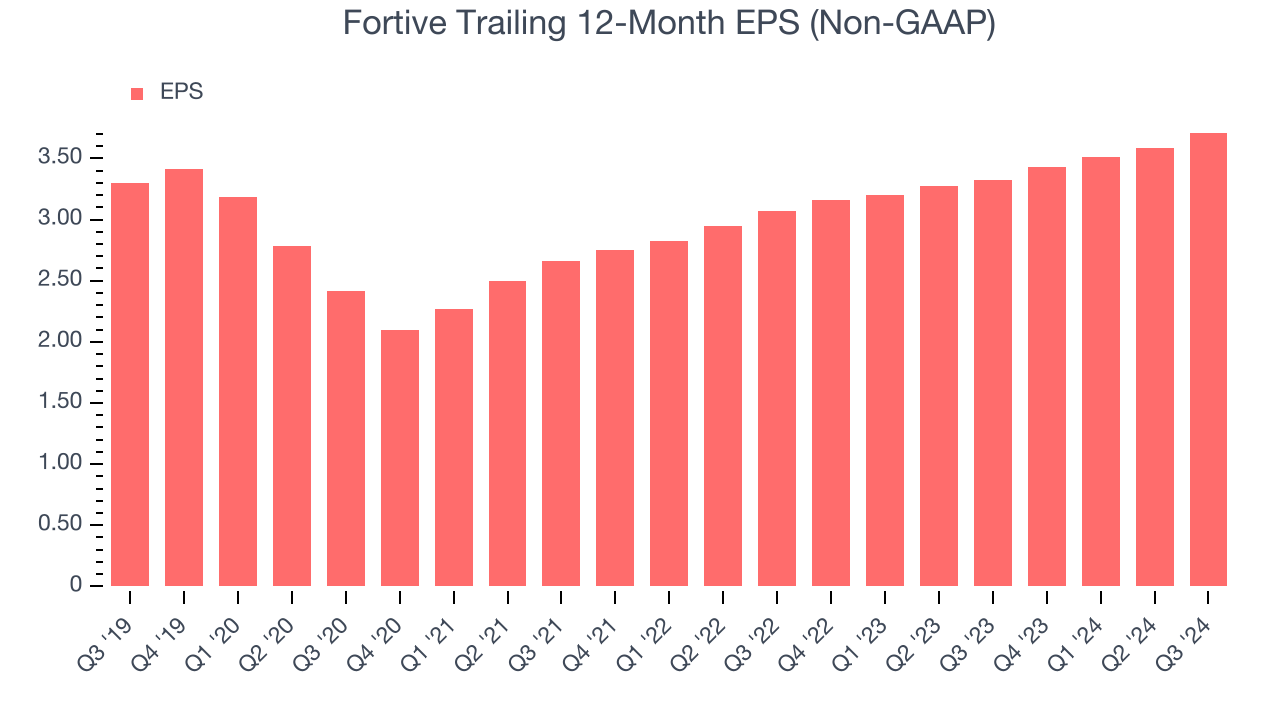

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Fortive’s EPS grew at a weak 2.4% compounded annual growth rate over the last five years. On the bright side, this performance was better than its flat revenue and tells us management responded to softer demand by adapting its cost structure.

We can take a deeper look into Fortive’s earnings to better understand the drivers of its performance. As we mentioned earlier, Fortive’s operating margin was flat this quarter but expanded by 8.7 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Fortive, its two-year annual EPS growth of 9.9% was higher than its five-year trend. Accelerating earnings growth is almost always an encouraging data point.In Q3, Fortive reported EPS at $0.97, up from $0.85 in the same quarter last year. This print beat analysts’ estimates by 4.2%. Over the next 12 months, Wall Street expects Fortive’s full-year EPS of $3.71 to grow by 11%.

Key Takeaways from Fortive’s Q3 Results

We enjoyed seeing Fortive beat analysts’ full-year EPS guidance expectations. We were also glad its EPS outperformed Wall Street’s estimates. On the other hand, its revenue unfortunately missed and its full-year revenue guidance slightly fell short of Wall Street’s estimates. Overall, this quarter was mixed with revenue guidance likely weighing on shares. The stock traded down 1.1% to $73.79 immediately following the results.

So should you invest in Fortive right now?The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.