Logistics solutions provider Hub Group (NASDAQ:HUBG) missed Wall Street’s revenue expectations in Q3 CY2024, with sales falling 3.7% year on year to $986.9 million. The company’s full-year revenue guidance of $4 billion at the midpoint also came in 2.9% below analysts’ estimates. Its GAAP profit of $0.39 per share was also 18.9% below analysts’ consensus estimates.

Is now the time to buy Hub Group? Find out by accessing our full research report, it’s free.

Hub Group (HUBG) Q3 CY2024 Highlights:

- Revenue: $986.9 million vs analyst estimates of $1.06 billion (7.1% miss)

- EPS: $0.39 vs analyst expectations of $0.48 (18.9% miss)

- EBITDA: $88.84 million vs analyst estimates of $85.35 million (4.1% beat)

- The company dropped its revenue guidance for the full year to $4 billion at the midpoint from $4.15 billion, a 3.6% decrease

- EPS (GAAP) guidance for the full year is $1.90 at the midpoint, roughly in line with what analysts were expecting

- Gross Margin (GAAP): 10.5%, in line with the same quarter last year

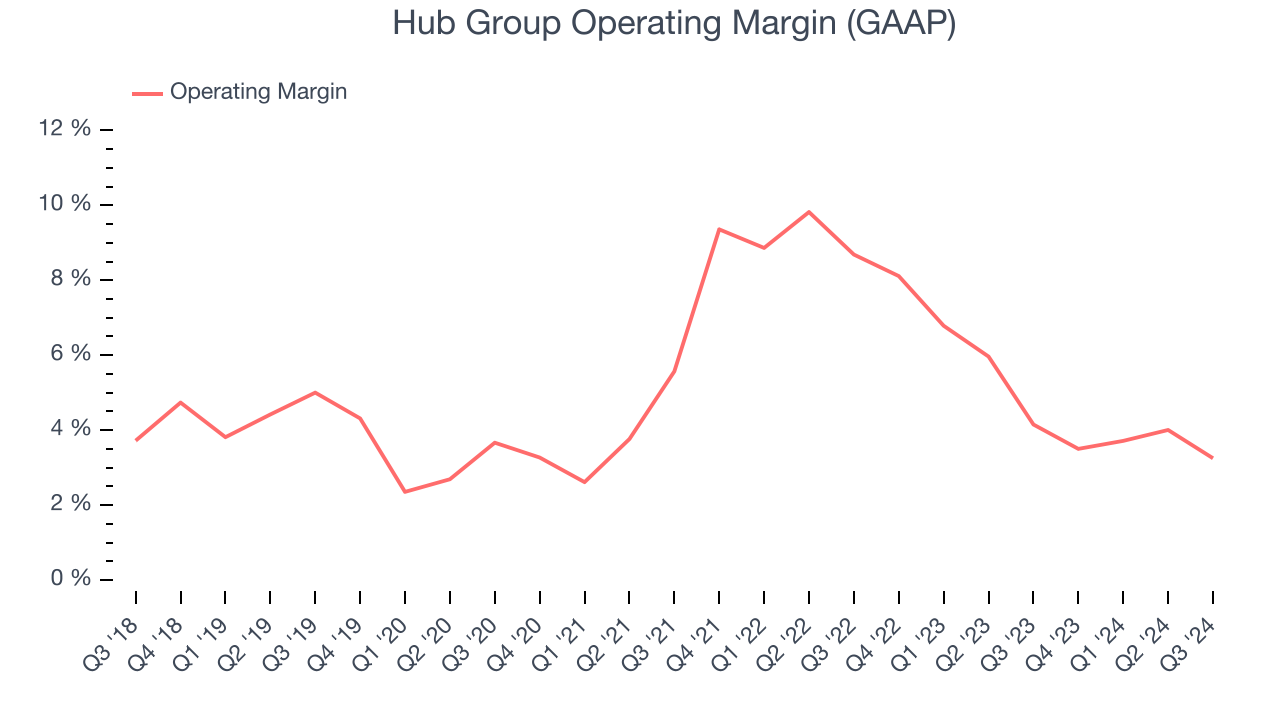

- Operating Margin: 3.3%, in line with the same quarter last year

- EBITDA Margin: 9%, in line with the same quarter last year

- Free Cash Flow Margin: 3.2%, down from 6.5% in the same quarter last year

- Market Capitalization: $2.70 billion

“I am pleased with the team’s performance in the third quarter as our disciplined market approach resulted in Intermodal volume growth of 12% and adjusted EPS growth in the quarter. In addition, we recently closed the joint venture with EASO to enhance our solutions for our customers and add significant scale to our Intermodal capabilities in Mexico. Although market conditions remain challenging, we continue to enhance earnings stability and growth over the long term by focusing on yield management, effectively managing costs, our capital structure, and providing excellent service to our customers,” said Phil Yeager, Hub Group’s President, Chief Executive Officer and Vice Chairman.

Company Overview

Started with $10,000, Hub Group (NASDAQ:HUBG) is a provider of intermodal, truck brokerage, and logistics services, facilitating transportation solutions for businesses worldwide.

Air Freight and Logistics

The growth of e-commerce and global trade continues to drive demand for expedited shipping services, presenting opportunities for air freight companies. The industry continues to invest in advanced technologies such as automated sorting systems and real-time tracking solutions to enhance operational efficiency. Despite the advantages of speed and global reach, air freight and logistics companies are still at the whim of economic cycles. Consumer spending, for example, can greatly impact the demand for these companies’ offerings while fuel costs can influence profit margins.

Sales Growth

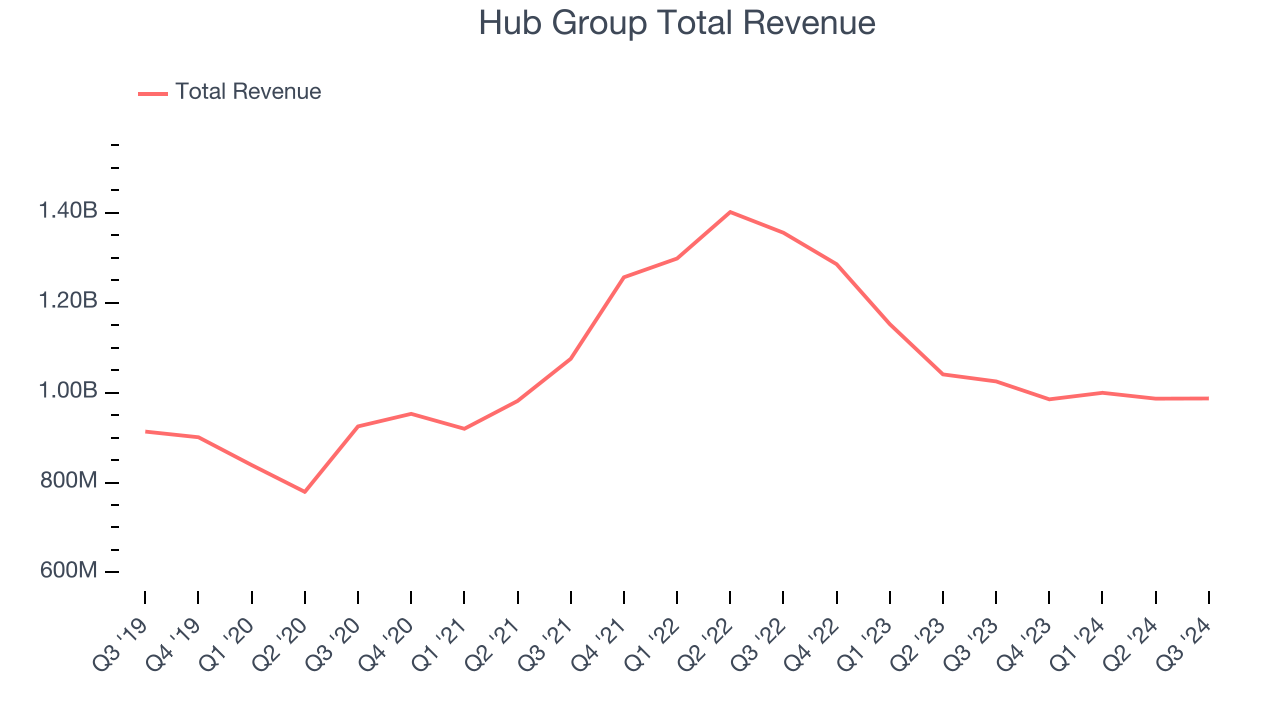

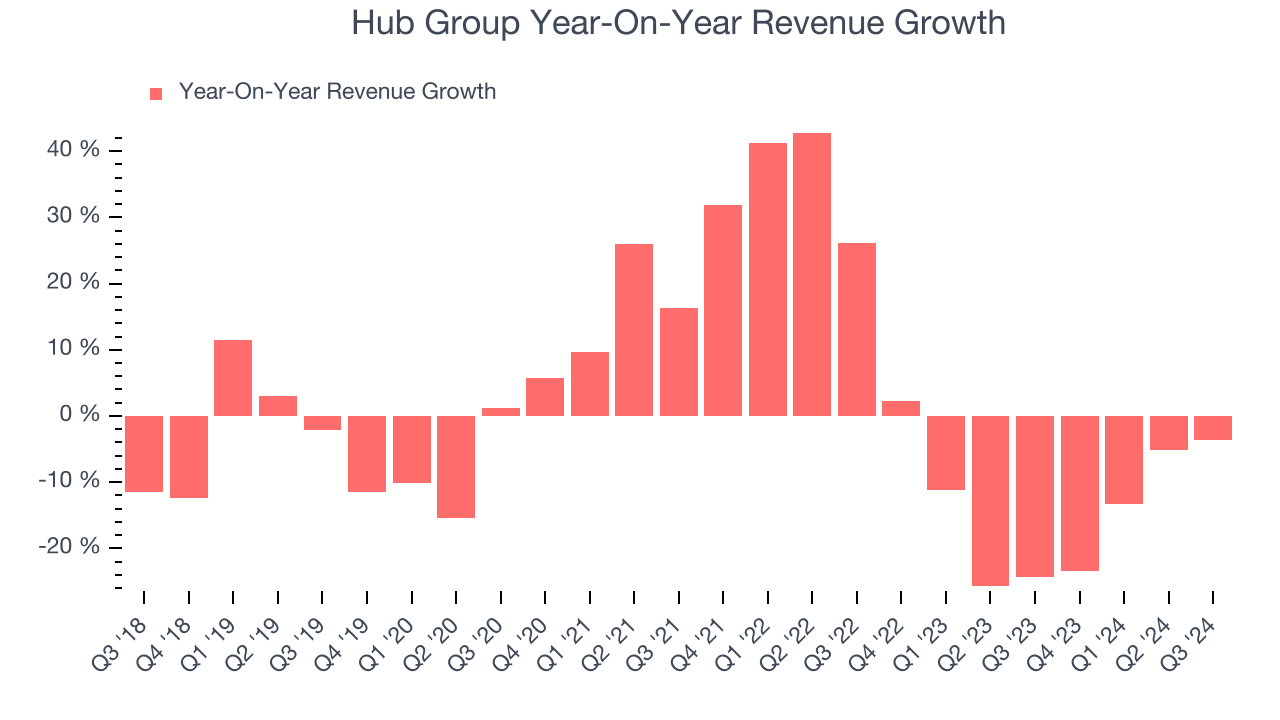

Reviewing a company’s long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one sustains growth for years. Hub Group struggled to generate demand over the last five years as its sales were flat. This is a tough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Hub Group’s recent history shows its demand has stayed suppressed as its revenue has declined by 13.7% annually over the last two years. Hub Group isn’t alone in its struggles as the Air Freight and Logistics industry experienced a cyclical downturn, with many similar businesses seeing lower sales at this time.

This quarter, Hub Group missed Wall Street’s estimates and reported a rather uninspiring 3.7% year-on-year revenue decline, generating $986.9 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 10.3% over the next 12 months, an improvement versus the last two years. This projection is noteworthy and illustrates the market thinks its newer products and services will spur faster growth.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Hub Group was profitable over the last five years but held back by its large cost base. Its average operating margin of 5.6% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Hub Group’s annual operating margin might have seen some fluctuations but has generally stayed the same over the last five years, meaning it will take a fundamental shift in the business to change.

In Q3, Hub Group generated an operating profit margin of 3.3%, in line with the same quarter last year. This indicates the company’s cost structure has recently been stable.

Earnings Per Share

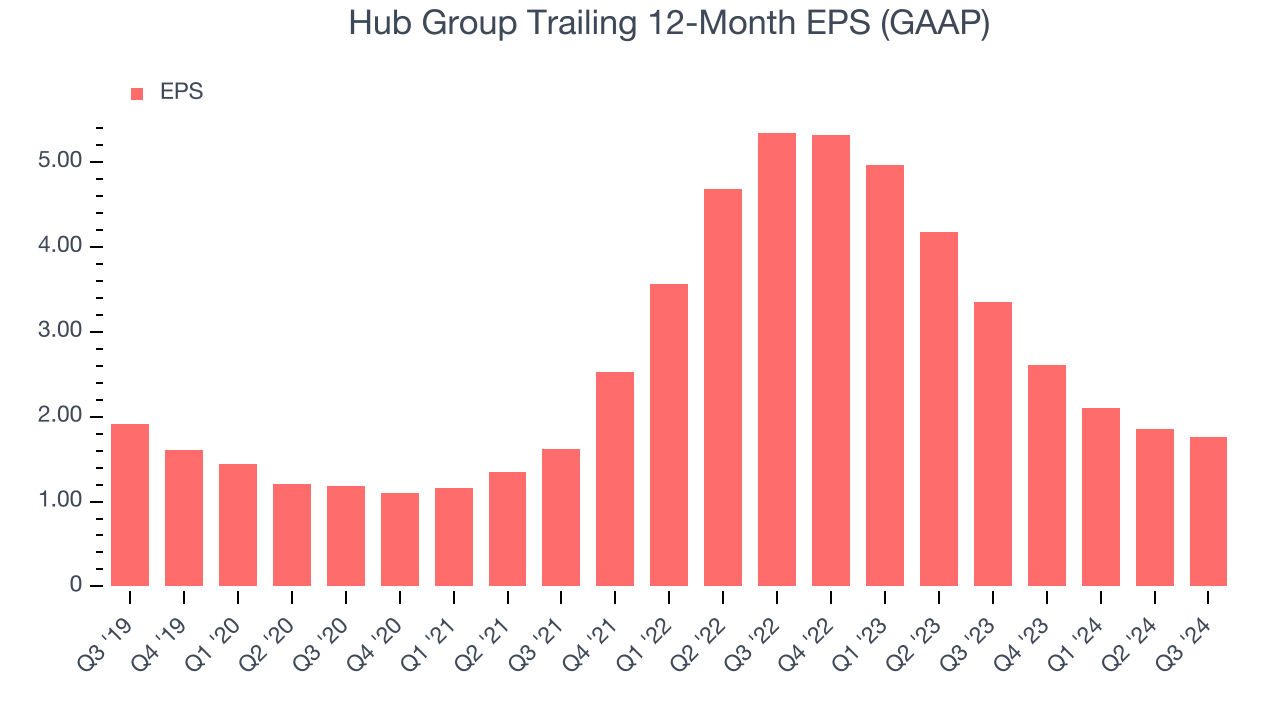

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth was profitable.

Sadly for Hub Group, its EPS declined by 1.6% annually over the last five years while its revenue was flat. This tells us the company struggled because its fixed cost base made it difficult to adjust to choppy demand.

Like with revenue, we analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business.

For Hub Group, its two-year annual EPS declines of 42.6% show it’s continued to underperform. These results were bad no matter how you slice the data.In Q3, Hub Group reported EPS at $0.39, down from $0.48 in the same quarter last year. This print missed analysts’ estimates. Over the next 12 months, Wall Street expects Hub Group’s full-year EPS of $1.76 to grow by 29.3%.

Key Takeaways from Hub Group’s Q3 Results

We enjoyed seeing Hub Group exceed analysts’ EBITDA expectations this quarter. On the other hand, its revenue missed and its EPS fell short of Wall Street’s estimates. Overall, this quarter could have been better. The stock remained flat at $43.75 immediately after reporting.

Is Hub Group an attractive investment opportunity at the current price?If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.